")

The bold and big thinking of Indian leaders is pushing India to become a $30 trillion economy in the next 30 years.

In a short span of a year, the Indian economy has quickly expanded, from the timely action of the RBI to tame inflation to expanding consumption – India is skyrocketing towards growth and development.

Recently, India has emerged as one of the most powerful countries, since it surpassed the UK to become the 5th largest world economy. However, a question is still being asked whether India can put itself forward as a $30 trillion economy.

Certainly, India holds the potential to become a $30 trillion economy which is clear from the fact that the nominal GDP (GDP at the current rate) has taken a big swing in the April-June quarter, i.e., Rs 64.95 lakh crores, according to the June rupee-dollar exchange rate it stands at $823 billion.

Moreover, it is also claimed that India surpassed the UK’s GDP in March itself, which was $813 billion, while India GDP was $864 billion.

However, as per 2021 April’s GDP outlook report of the International Monetary Fund (IMF), India’s GDP ($3.18 trillion) was right behind UK’s GDP ($3.19 trillion) in 2021. Conversely, it has also been anticipated that India would become a $3.54 trillion economy by the end of 2022 if compared to the UK’s projected GDP which would be $3.38 trillion.

From the estimated data and India GDP growth, it can be seamlessly prognosticated that India will soon become a $3.54 trillion economy by the end of 2022 considering its present growth.

Although, in which year it can become a $30 trillion economy will depend on many factors.

With that, let’s see some facts, how the India GDP surpassed the GDP of the UK?

How India GDP Growth Has Surpassed the UK

The timing could not have been more auspicious when India emerged as the 5th largest world economy at midnight after the entire country celebrated Azadi ka Amrit Mahotsav, that’s its 75th Independence day. Moreover, after overtaking the UK, India is all set to skyrocket to be the third-largest world economy by 2029.

The path taken by India since 2014 reveals it is likely to get the tag of the third largest economy in 2029, a movement of seven places upward since 2014 when India was ranked 10th. India should surpass Germany in 2027 and Japan by 2029 at the current rate of growth (as per estimated figures).

From the estimated data, it can be safely projected that India has been moving in the right direction, and we can conclude that India GDP rank will surpass the world economic leaders in the coming years.

How India pipped the UK, our colonial rulers –

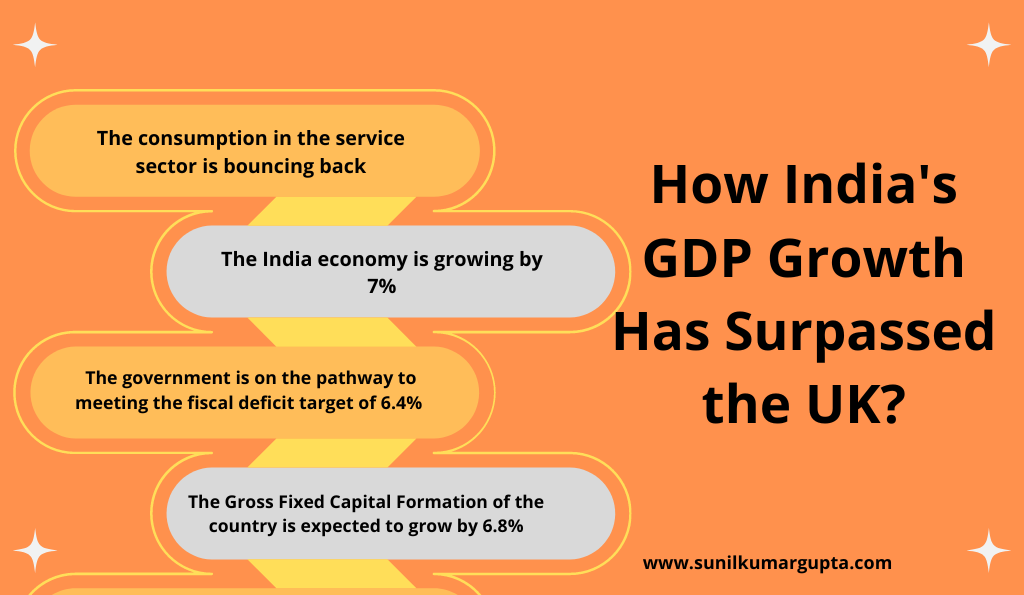

- Due to pent-up demand, the consumption in the service sector is bouncing back, as consumers are stepping out and spending (as per 2019-2020 data). One of the major reasons for the increase in demand is the “ abundance of festivals” celebrated in India.

- While the world is on the brink of recession, our economy is growing by 7%.

- As per the Finance Secretary, the government is on the pathway to meet the fiscal deficit target of 6.4% (Rs. 16, 61,196 crores) in the current fiscal year ending in March 2023, while currently, it is Rs. 15, 91,089 crores as per revised estimates for 2021-22.

- The Real Gross Fixed Capital Formation of the country is expected to grow by 6.8% (2021-22), previously it was -9.8 (2020-21).

Yet, with the commendable achievement of India, one aspect which can not be ignored is, that “the per capita income of India is low, as India ranked 144 positions out of 190 countries.”

It indicates a clear picture of poverty, income disparity, and our inability to account for inflation, wealth, or saving, therefore, even after achieving the milestone of being recognized as the “world’s fifth largest economy” the Indian economy is lagging behind in distinct aspects.

Whether India Will Be Able to Transform Itself Into a $30 Trillion Economy or Not | India GDP Growth

India GDP growth in the last 10 years, reflects a meritorious change, as it jumps to 8.9% in 2021 from 5.5% in 2012, especially after sinking as low as -6.6% in the previous year.

With the magnificent elevation in GDP of India, it can unequivocally be noticed that we are perfectly poised on the passageway to aspire to be a $30 trillion economy in the next 30 years. Though, it seems like a far-fetched dream, yet, beyond doubt it’s not rocket science as with our magical power of demographic dividend, youth power, and power of democracy – India can proudly establish itself as a $30 trillion economy.

Although, India encounters varied stumbling blocks to be finally crowned as a $30 trillion economy, such as –

The Economic Issues in India

1. Low Per Capita Income

Even after 75 years of Independence, India continues to be a developing country, whose one feature is low per capita income. However, in 2020-21 low per capita income has dropped to Rs 1.27 lakh from Rs 1.32 lakh in 2019-20, while in 2021-22 it is estimated to be 1.50 lakh.

Apart from this, the problem of unequal distribution of income exists in India, which is one of the significant contributors and obstacles to economic development.

Proposed solution –

- Increase in farmers’ income – India’s 54.6% of the population works in the agriculture sector and historically, India has always kept prices of agricultural products low. However, due to the introduction of schemes like the Farm Acts, the Indian government can allow farmers to earn high profits. Therefore, with the increase in profit of farmers, they can provide support to the other economic sectors through their consumption. For instance, products like fertilizers, working attire, and tools are a necessity for farmers, especially if they are planning to expand their business. So, this increase in expenditure will generate more job opportunities.

- Urbanizing India’s rural population – Urbanization drives growth, due to the prominent nature of the Indian agricultural population, moving certain farmers into rural areas could allow them to generate employment and increase agricultural productivity by minimizing the working of a number of farmers on the same land. Therefore, it will help in growing India’s medium-sized cities. Moreover, the Indian government can promote migration by providing incentives to farmers, including investment in infrastructure development and urban services. Further, the new urban population will generate a resurgence of the housing market and provide more lending opportunities to banks. This in return will result in more development and urbanization, thus, would create more international investment and manufacturing export opportunities.

2. Dependence on Agriculture

Over 54.6% of the population is dependent on agriculture to earn a livelihood, which only contributes 20.2% to the national income, reflecting low productivity. Fortunately, in the Union Budget 2022-23, Rs 1.24 lakh crores have been allocated to the Department of Agriculture, Cooperation, and Farmers’ Welfare.

The measures are taken by the government, such as financial and the introduction of policies, positively solve the problem of individuals working in the agriculture sector.

Proposed solution –

- Technological advancement – Apart from increasing the farmers’ income and urbanizing India’s rural population (earlier mentioned points), the Indian government can emphasize on the introduction of technologies in agriculture. Since, technology can assist farmers in predicting the climate, decreasing water usage, increasing yield, and their net profit margins. That in return increases India GDP growth rate.

- Digital Credit Policy – Though the Indian government has already launched several credit policies to ensure easy access to loans with fewer legal formalities, yet, farmers could not able to avail the benefits of credit. That could be solved by combining easy access to loans with a digital credit policy, under which loan filing would become much simpler.

3. High Population

Another factor, which is the stumbling block in economic development is heavy population pressure. Contemporary, India is the second most populous country, after China, yet, the per capita income of our country is low, which results in income disparity, and the inability to account for inflation, wealth, or saving.

Further, in order to take care of the well-being of the population of the country, the government has to allocate high funds to fulfill basic requirements like food, shelter, medicine, schooling, electricity, hygiene, and more.

Proposed solution –

- India can put more emphasis on programs like “AI for Youth” under which youth will be trained to be future-ready for AI development. Therefore, will commence the trend of entrepreneurship and contribute to India GDP growth.

- To create “future entrepreneurs” the government can put more emphasis on the improvement of the soft skills of a student which are core for all professionals, rather than emphasizing on traditional studying methods.

- Preventing the migration of India’s youth to other countries (to search for better opportunities) can be done through the creation of better jobs in all sectors.

- The Indian government could provide subsidiaries to scientists, engineers, and other students (youth) who persist in talents but lack financial support.

- Females/ women should be prepared to lead the fields which are considered non-fit for them, that’s how we will have another Sarla Thukral, Mithali Raj, and more.

4. Existence of Under-employment And Chronic Unemployment

Unemployment of any kind is a curse of any economy, be it developed or developing, and being a developing country, India is also encountering similar problems. Therefore, due to the abundance of labor, it is challenging for the government to generate employment opportunities for the entire population.

In addition to that, due to a deficiency of capital, secondary and tertiary occupations are inadequate, which results in under-employment and chronic unemployment.

Proposed solution –

- Unemployment is a constant problem in the Indian economy and the Indian government has introduced several schemes to minimize unemployment such as Atmanirbhar Bharat Rojgar Yojana, Pradhan Mantri Rojgar Protsahan Yojana, etc. However, India’s world-beating growth is not creating as many jobs, considering that India should put more emphasis on improving the education system and job training.

- Even though the employment rate has increased, employers couldn’t hire due to a lack of skills in freshers. Therefore, there is a need to give importance to the soft skills of students.

- The Indian government can invest in the establishment of more industries and infrastructure development projects to minimize under-employment.

- Training in the workplace, youth employment services, and career education could be a great way to improve skills, create more entrepreneurs, and allow students to choose the right career.

5. Leisurely Improvement in Rate of Capital Formation

From the beginning, one thing that pertains is a deficiency of capital in India, though, in 2021-22, the Gross Fixed Capital Formation of the country is expected to grow by 6.8%. Therefore, reflecting positive growth, yet, considering the high population growth, India could use better measures to increase the rate of gross capital formation.

Proposed solution –

- Saving and investment from household savings or government policy need to be increased by improving the money flow, that in return increases the private investment or fixed asset acquisition. Therefore, increase in gross fixed capital formation.

- Resident enterprises in the country can be increased to increase the gross fixed capital formation. For instance, oil extraction occurs in open seas, so the associated fixed capital is allocated to the national territory, in which the relevant enterprises are resident.

The mentioned economic issues have many potential solutions (as mentioned above) and it is no doubt that with time India has made progress in many fields.

Certainly, from the 5 worst economies in the world to the world’s 5th largest economy, India has truly proven it’s worth and how its leaders have been working in all directions to tame the world to see India growing and expanding as a world power.

What Are The Strengths Of The Indian Economy?

India, the fastest growing economy has to realize the strengths of demographic dividend, youth power, and the power of democracy. It is no doubt, from the year 2014 to 2022, India has witnessed tremendous growth in distinct aspects – be it science and technology, innovation, agriculture, the service sector, or digitalization.

Under the leadership of Hon’ble PM Modi Ji, India has built a modern economy, lifted millions of individuals from poverty, become a space and nuclear power, and developed robust foreign policies.

Since 2014, India has come a long way, leaving a string of landmarks, which defines its journey. This section of the blog will trace the strengths of the Indian economy and India will become a $30 trillion economy.

1. Mixed Economy

The Indian economy is a perfect example of a mixed economy, which means private and public both sectors co-exist in India and function smoothly. On one hand, the public sector operates on heavy and fundamental industries, while on the other hand, private sectors have gained importance (due to liberalization).

That provides a model for a “public-private partnership” where both, private and public sectors can work together through the adequate contribution of financial resources, management expertise, technology, and other resources.

2. An Emerging Market

India has emerged as a vibrant economy, which contributes to the stable the India GDP growth rate, even amidst global downstream, India continues to show positive India GDP growth trends, especially with the introduction of policies such as an automatic route for FDI in India, including measures taken by the government to attract domestic and foreign investment such as –

- Empowered Group of Secretaries (EGoS) Project Development Cells (PDCs)

- Production Linked Incentive (PLI) Schemes

- PLI Scheme

- Make in India

- Investment Clearance Cell (ICC)

- One District One Product (ODOP) and more.

All the initiatives taken by the Indian government reflect the high prospect for growth.

3. Expansion in The Role of Agriculture

As mentioned, the largest part of our population is engaged in agriculture, which also contributes to the India GDP growth of the country. The introduction of the “green revolution” and other “bio-technological” improvements in agriculture has made Indian agriculture more efficient and has increased the surplus too.

Including that, government initiatives such as PM Fasal Bima Yojana (PMFBY) (provides insurance on naturally grown crops,) Paramparagat Krishi Vikas Yojana (PKVY), and National Project on Organic Farming schemes – have pushed our agriculture sector towards growth. Moreover, PM Modi Ji’s government has also been working to incorporate AI in agriculture, which will again be an immense step towards development.

4. Service Sector

Due to liberalization and economic reforms India’s service sectors are flourishing, especially with the introduction of schemes like Make in India, and Digital India Mission, including schemes to boost the “12 champion service sectors” that are IT & ITeS, Tourism, and Hospitality, Medical Value Travel, Transport and Logistics, Accounting and Finance, Audio Visual, Legal, Communication, Construction, and Related Engineering, Environmental, Financial and Education – India is truly making immense progression in the service sector.

The service sector is the largest sector in India, estimated to grow by 8.2%.in 2021-22, after a contraction of 8.4% the previous year.

5. Demographic Dividend

The human capital of India is young, which reflects that India is a proud owner of the maximum percentage of youth. The “youth” is not only highly motivated but also the greatest asset of a country, if skilled and trained adequately. And in order to provide diversified training to the youth, Hon’ble PM Modi Ji’s government has introduced schemes such as –

- Pradhan Mantri Kaushal Vikas Yojana (PMKVY)

- Craftsman Training Scheme (CTS)

- Pradhan Mantri Kaushal Kendras (PMKK)

- Scheme for Higher Education Youth in Apprenticeship and Skills.

- National Apprenticeship Promotion Scheme.

- National Programme for Civil Services Capacity Building.

- Green Skill Development Programme.

With the introduction of such programs and schemes, the Indian government is constantly taking measures to train and enhance the skills of youth, in order to create human capital to maximize the growth prospects of the country.

Moreover, the availability of maximum human capital in India attracts investment opportunities in India, hence, contributes India GDP growth.

6. High Purchase Price Parity (PPP)

Purchase Price Parity (PPP) refers to the rates of currency conversion, which tries to equalize the purchasing power of other currencies by obliterating the differences in price levels between countries.

The PPP of India stood at 23.14 in 2021, which reflects that India is one of the countries with the highest PPP. That means that the same product would cost less in India, than in other countries, for instance, the price of the same shoes would be high in the US, say $50 (3,982.53), however, would say Rs 2000 in India.

This opens up the possibility of exports to other countries, since raw materials are economical in India, thereby contributing to the India GDP growth.

7. Rapid Growth of Urban Areas

Urbanization is one of the keys to improve the growth of the economy and under the leadership of Hon’ble Narendra Modi Ji several measures have been taken to provide distinct facilities in rural areas such as electricity, schools, employment, banks, and financial institutions, transportation facilities, and more.

Along with that, more scheme has been introduced with the purpose to ensure further development, such as –

- Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS)

- Shyama Prasad Mukherji Rurban Mission (SPMRM)

- Aadarsh Gram Yojana (AGY) :- SAGY, VAGY & SPAGY.

- Pradhan Mantri Adarsh Gram Yojana (PMAGY)

- Pradhan Mantri Jan Vikas Karyakram (Center 60 : State 40)

- Swaranjayanti Khand Utthan Yojana (100 % State

8. Digitalization

Digitalization in India, once a traditional country, is now a home of AI system designers and will soon become an AI hub, especially when the government is taking adequate measures to support digitization. India stands 4th in the largest producer of AI-relevant scholarly papers and has introduced initiatives like AI for Youth (commenced in 2020) to make the youth future ready for AI developments.

Apart from that, our hon’ble PM also talks about making work from home a reality, which will allow more women to participate in the workforce, ensure energy saving, and will allow youth to manage studies and work conveniently.

9. Science and Technology (AI)

India is among one of the top countries in the world and in order to be successful in science and technology, the Indian government has launched schemes like INSPIRE “Innovation in Science Pursuit for Inspired Research” or “Abdul Kalam Technology Innovation National Fellowship”, and other schemes with the purpose to encourage innovation in this sector.

It is no doubt that India is prosperously achieving success through launching Mission mars, or GSAT- 19.

10. Startup Hub

With the introduction of startup culture in India, India is becoming a startup hub, since due to schemes introduced by the Indian government, now startups are receiving concessions, subsidiaries, and more.

Some of the schemes are –

- Pradhan Mantri Mudra Yojana.

- Credit Guarantee Trust Fund for Micro & Small Enterprises (CGTSME).

- Financial Support to MSMEs in ZED Certification Scheme.

- Credit Linked Capital Subsidy for Technology Upgradation (CLCSS).

- Design Clinic for Design Expertise to MSMEs.

Conclusion

India has overthrown one of the cultural, technological, and scientific leaders by conquering the position of the world’s fifth-largest economy, thereby, reflecting an increase in India GDP growth.

India has always strived hard to adopt the best possible measures and strategies, which are in the interest of the economy as a whole and which have wider political and economic implications for the country and the world. From our track record, we envision the path of a $30 trillion economy, through a constant emphasis on fair and credible policies and measures that will eliminate unemployment issues, improve technological development and infrastructure, ensure adequate utilization of economic resources, and other aspects associated with economic development.

Moreover, under the guidance of our honorable Prime Minister Narendra Modi, India will soon become a $5 trillion economy and will head strategically on the path to becoming a $30 trillion economy.

Written & Compiled by CA Sunil Kumar Gupta

Founder Chairman, SARC Associates

0 Comments